Retirement Planning • Inflation • Market Volatility

Inflation Has Been Stubbornly High.

How Higher Prices Can Pressure Retirement Income

3 Key Takeaways

1

Even moderate inflation can significantly increase retirement expenses over a 20–30-year retirement.

2

Higher inflation combined with market volatility can create additional pressure on retirement portfolios.

3

Running inflation, bear market, and withdrawal strategy scenarios can help retirees better prepare for uncertain economic conditions.

Want to see how inflation could affect your retirement over time?

Run retirement scenarios in WealthTrace to model higher inflation, market downturns, changing spending needs, and different withdrawal strategies so you can see how your plan may hold up under pressure.

Start Free Trial

Test your retirement plan under inflation pressure.

Recent inflation data showed consumer prices rising again in April, reminding many retirees and pre-retirees that inflation remains one of the biggest long-term risks to retirement plans.

While a single inflation report does not necessarily indicate a major economic shift, persistent higher prices can quietly erode purchasing power over time — especially during retirement.

For retirees living on withdrawals, Social Security, pensions, and investment income, inflation can have a significant impact on long-term financial security.

U.S. inflation has remained volatile over the past decade, highlighting the importance of building flexibility into long-term retirement plans.

Inflation Can Quietly Erode Retirement Spending Power

Retirement planning is not just about growing investments. It is also about maintaining purchasing power throughout retirement.

A plan that appears successful today under lower inflation assumptions may look very different if inflation remains elevated for several years.

Many retirees underestimate how much inflation compounds over time. For example, a household spending $80,000 per year today would need to spend over $107,000 annually in just 10 years if inflation averaged 3% per year.

At higher inflation rates, those increases become even more dramatic.

Healthcare costs can be particularly sensitive to inflation. Medicare premiums, out-of-pocket medical expenses, insurance costs, and long-term care expenses may all rise faster than general inflation over time.

Retirees often feel these increases more directly because they are living on fixed income sources or portfolio withdrawals.

Inflation can also create additional stress during periods of market volatility. If retirees are withdrawing larger amounts from investment accounts to keep up with rising costs while markets are declining, portfolio sustainability can become more difficult.

This is commonly referred to as sequence-of-returns risk.

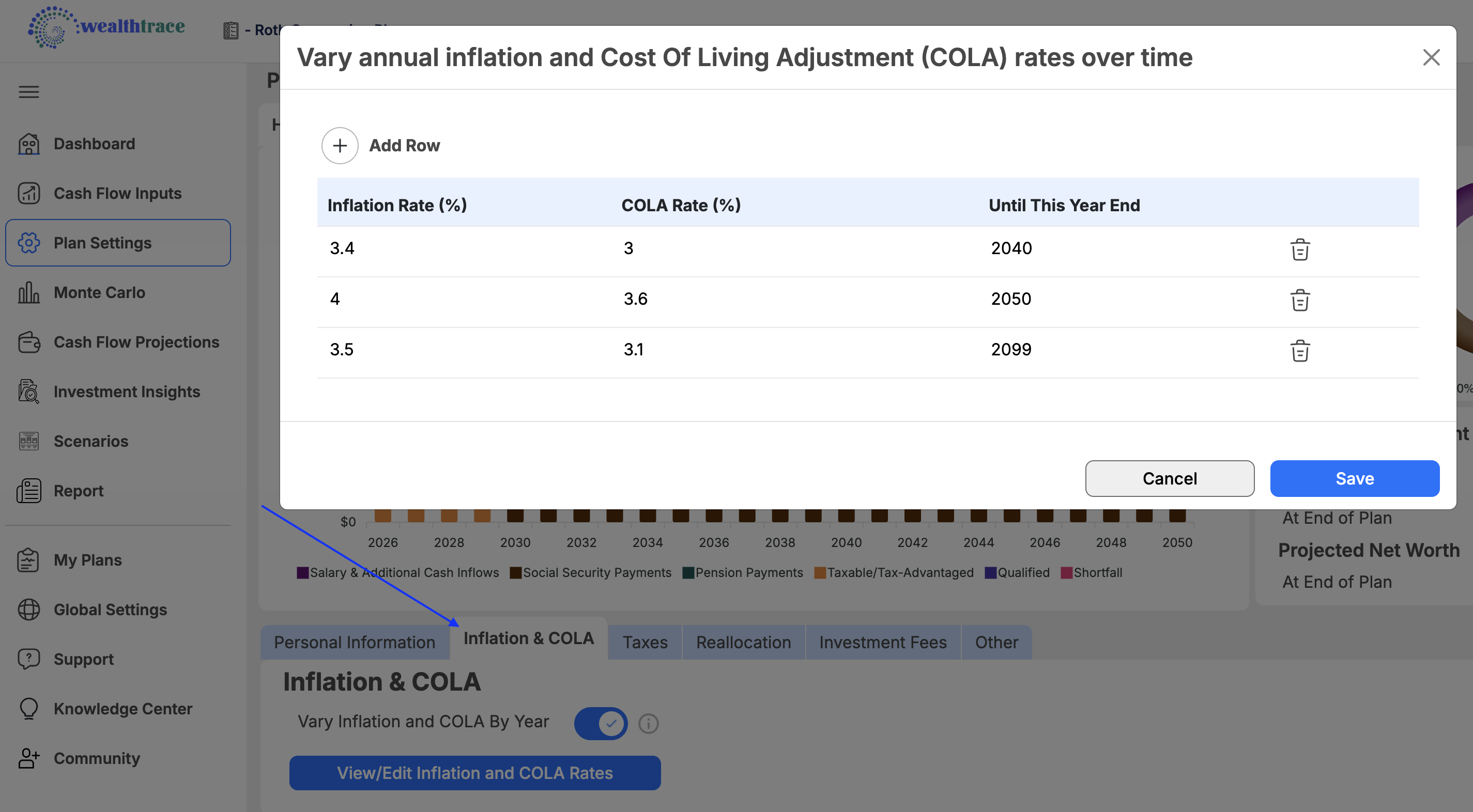

WealthTrace Planning Tip: Adjust future inflation assumptions under Plan Settings to see how higher inflation rates could impact long-term retirement projections and overall plan success rates. You can also customize inflation rates for specific goals and cash inflows to create more detailed and realistic planning scenarios.

Stress Testing Matters More During Uncertain Economic Conditions

One of the most important things retirees can do during uncertain economic environments is stress test their retirement plans.

Rather than relying on a single projection, it can be helpful to model different scenarios to better understand how changing market conditions, inflation, and spending levels could affect long-term outcomes.

For example, retirees may want to evaluate:

- Higher long-term inflation assumptions

- Historical recession scenarios

- Different retirement spending levels

- More conservative asset allocations

- Tax-efficient withdrawal strategies

This type of scenario analysis can help retirees identify potential weaknesses in their plans before economic conditions worsen.

Bear markets can become even more difficult when combined with elevated inflation. During major historical recessions, retirees often experienced both portfolio declines and rising living costs simultaneously.

This combination can place additional pressure on withdrawal strategies and portfolio longevity.

Running historical bear market scenarios can help retirees better understand how their plans may perform during difficult economic periods.

Instead of assuming smooth market growth, these scenarios allow investors to evaluate how retirement plans hold up during periods similar to past recessions and market downturns.

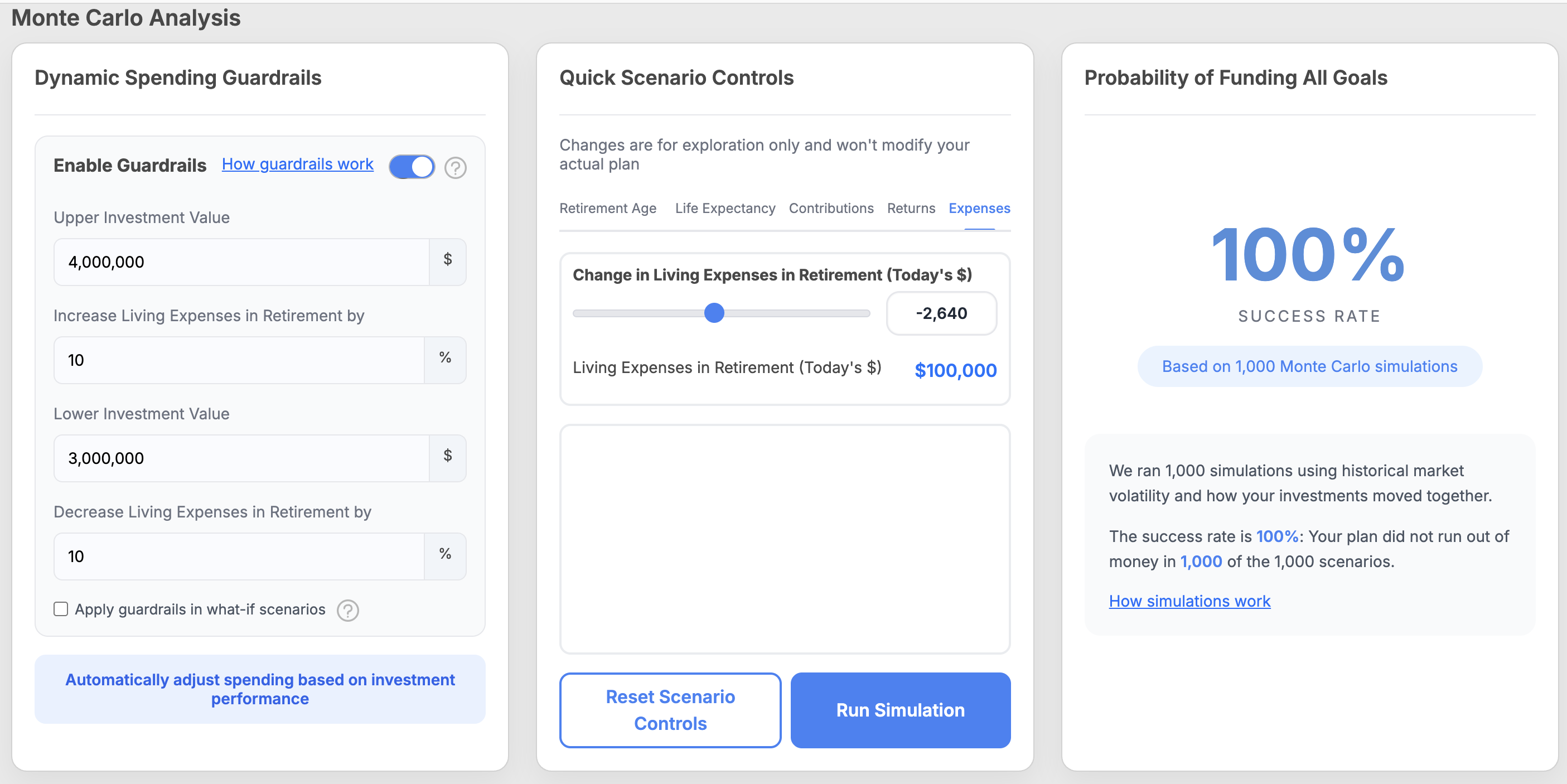

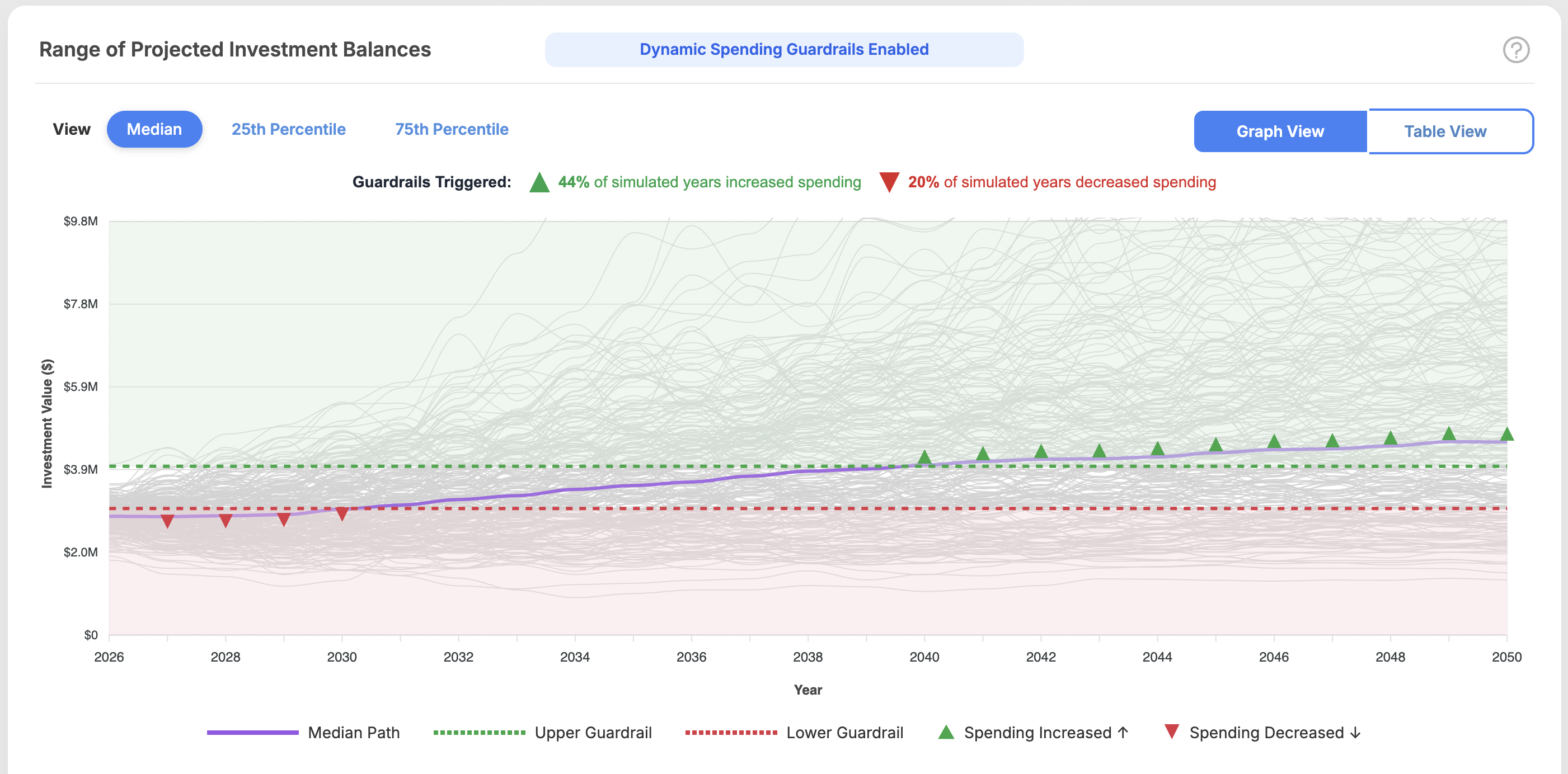

WealthTrace Planning Tip: Monte Carlo simulations in WealthTrace incorporate historical market behavior, including past recessions and bear markets, across 1,000 different scenarios. This can provide a more realistic indicator of retirement plan success compared to a simple linear projection using static returns. You can also apply Spending guardrails to model spending adjustments during market upturns and downturns and run quick scenarios to instantly test changes such as reducing annual spending.

Inflation Can Also Affect Retirement Taxes

Inflation can also affect taxes in retirement. As retirees withdraw larger amounts to cover rising expenses, taxable income may increase over time.

This can potentially affect Medicare IRMAA surcharges, taxation of Social Security benefits, and overall lifetime tax exposure.

For some retirees, Roth conversion strategies may become even more valuable during periods of uncertainty.

Strategic Roth conversions may help reduce future required minimum distributions (RMDs), create tax diversification, and potentially improve long-term retirement flexibility.

Withdrawal order can also play a major role in retirement outcomes.

Drawing funds from accounts in a tax-efficient order may help retirees reduce lifetime taxes and preserve portfolio longevity.

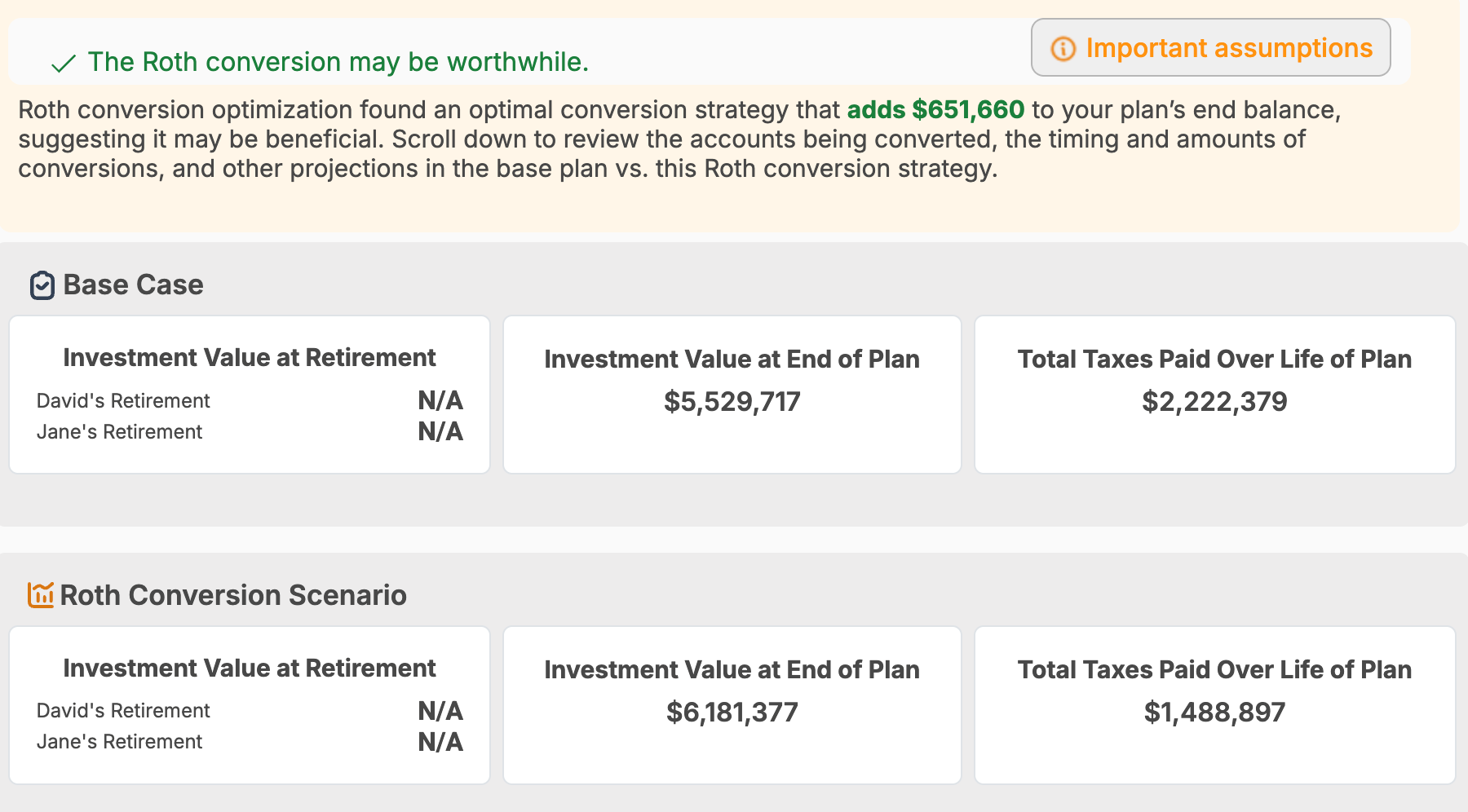

WealthTrace Planning Tip: Run Roth conversion scenarios, tax projections, and withdrawal order analysis to evaluate more tax-efficient retirement income strategies. The Roth Conversion Optimizer can also help calculate potentially optimal conversion strategies based on your retirement goals and long-term projections.

See how higher inflation and market stress could change your retirement plan.

WealthTrace helps you test higher inflation assumptions, recession scenarios, tax strategies, and withdrawal approaches so you can build a more flexible retirement plan.

Start Free Trial

Stress-test your retirement plan instantly.

Summary

Inflation remains one of the most important long-term risks retirees face. Even moderate increases in living costs can significantly affect retirement spending needs over time, especially when combined with market volatility.

Retirees should consider stress testing their plans using higher inflation assumptions, historical bear market scenarios, tax projections, and different withdrawal strategies.

Tools like WealthTrace can help investors evaluate how changing economic conditions may affect long-term retirement success and identify opportunities to improve flexibility and resilience in retirement plans.