Retirement Planning • Medicare • Social Security

Managing IRMAA in Retirement

Smart Income Strategies to Keep More of Your Benefits

3 Key Takeaways

1

Medicare IRMAA can reduce your net Social Security payment because higher-income retirees pay more for Medicare Part B and Part D.

2

IRMAA is based on income from two years earlier, so one-time income spikes can raise premiums long after they occur.

3

With proper income planning—including Roth conversion timing and capital-gain management—retirees can often limit these surcharges.

Want to see your IRMAA risk before it hits your Social Security check?

Run a quick retirement income plan in WealthTrace and instantly see how Roth conversions, capital gains, and RMDs may affect Medicare premiums—year by year.

Start Your Free Trial

Explore planning scenarios.

Many retirees expect their Social Security benefit to steadily rise with cost-of-living adjustments (COLAs). Yet each year, some beneficiaries notice their deposit barely increases—or doesn’t increase at all.

Often, the reason isn’t

Social Security.

It’s Medicare.

Medicare

Part B and Part D premiums are typically deducted directly from your monthly Social Security payment. When those premiums rise, especially due to IRMAA (Income-Related Monthly Adjustment Amount), your take-home benefit can shrink even while your official Social Security benefit increases.

For higher-income retirees, IRMAA can add hundreds of dollars per month in additional premiums.

And the most confusing part:

The premium increase is based on income you earned two years ago — not your income today.

How IRMAA Works

Medicare sets a standard premium each year for Part B (medical insurance) and Part D (prescription drug coverage). Retirees whose income exceeds certain thresholds must pay additional premiums through IRMAA.

For IRMAA, Medicare uses a version of Modified Adjusted Gross Income (MAGI). This is generally your Adjusted Gross Income (AGI) from your tax return plus tax-exempt interest. As a result, income Medicare considers can be higher than many retirees expect.

The Social Security Administration uses the most recent tax return information provided by the

IRS,

typically income from two years earlier, to determine your premium level.

For 2026 Medicare premiums, IRMAA begins when 2024 income exceeds $109,000 for single filers or $218,000 for married couples filing jointly, with higher tiers above those levels. Because IRMAA works in brackets, even a small increase in income can push you into a higher premium level for the entire year.

Your Social Security benefit may go up on paper—but your spending money may not.

Why Past Income Still Matters

Because IRMAA uses a two-year lookback, income spikes late in your career or early in retirement can affect premiums well after income falls.

Common triggers include:

- Large capital gains from selling investments

- Exercising stock options

- Selling a business or rental property

- A final high-income working year or severance

- Significant Roth conversions

Life changes can also increase exposure. After a

spouse dies,

the survivor usually shifts from Married Filing Jointly to Single status. Since IRMAA thresholds for single filers are much lower, the same income can suddenly trigger higher premiums.

From a WealthTrace user

“We haven’t reached Medicare age yet, but we’ve already experienced several ‘phantom income’ events—selling a rental property, Roth conversions, and inherited IRA RMDs. The income showed up on our tax return even though our actual cash flow didn’t really change.”

Shared with permission. Individual experiences vary.

3 Actionable Steps for Retirement Income Planning

1

Shift Toward Income That Doesn’t Increase MAGI

Because IRMAA is based on MAGI, the type of income you withdraw matters.

Roth IRA withdrawals

Qualified Roth withdrawals

are tax-free and generally do not increase MAGI, meaning they typically don’t affect IRMAA.

Roth conversions (the key planning tool)

A

Roth conversion

is taxable in the year it occurs and can temporarily raise Medicare premiums two years later. However, many retirees intentionally convert during the early retirement years—before Social Security and before Required Minimum Distributions (RMDs) begin—when taxable income can be unusually low.

Converting portions of a traditional IRA during this window can:

- Reduce future RMDs

- Lower lifetime tax rates

- Help prevent recurring IRMAA surcharges later

- Create tax-free income in later retirement

In other words, a planned conversion may create a small, temporary IRMAA increase in exchange for avoiding larger, permanent increases in your 70s and 80s.

Without planning, RMDs beginning at age 73—combined with

Social Security

and withdrawals—often push retirees into higher IRMAA tiers every year thereafter.

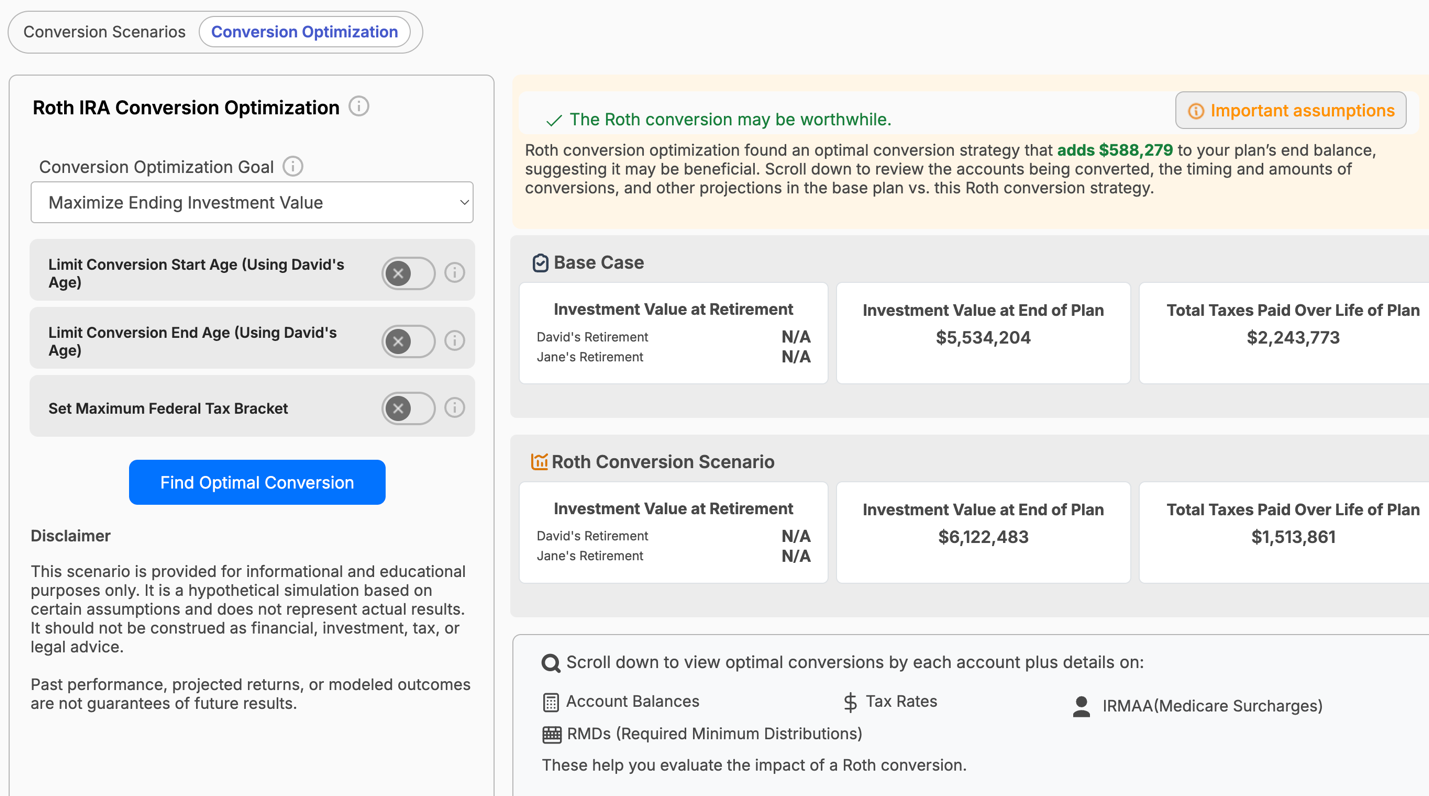

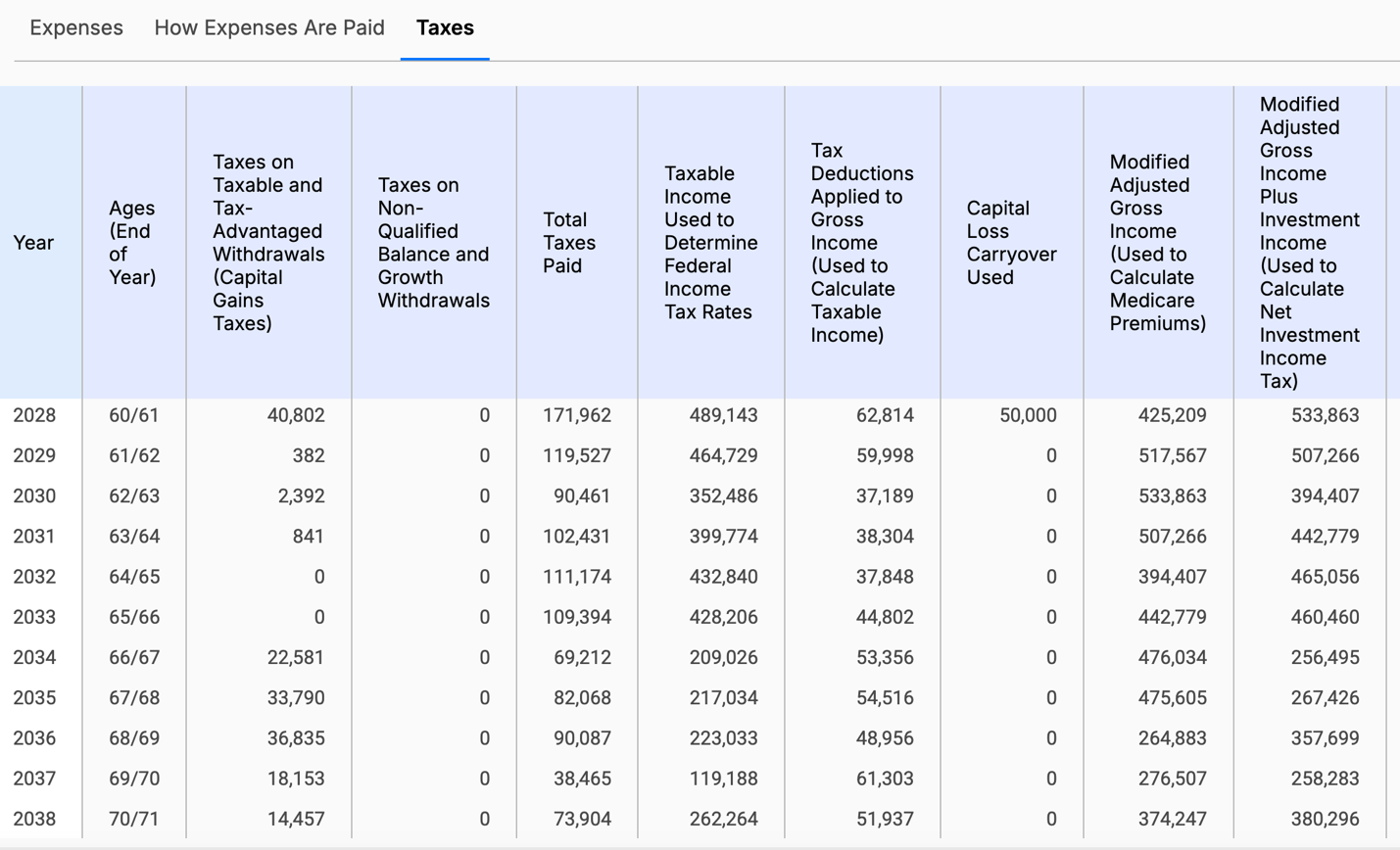

Example: Roth conversion scenario modeling and projected Medicare premium impact.

Example: Roth conversion scenario modeling and projected Medicare premium impact.

WealthTrace Planning Tip: WealthTrace lets you run Roth conversion scenarios and instantly see the impact on Medicare premiums today and in future years. Test amounts manually or use the optimizer to find an efficient conversion strategy.

Health Savings Account (HSA) withdrawals

HSA

distributions for qualified medical expenses are also tax-free and excluded from MAGI.

By increasing tax-free income sources later in retirement, retirees gain more control over both taxes and Medicare premiums.

2

Be Strategic with Capital Gains

Capital gains are one of the most common accidental IRMAA triggers. Even though long-term gains receive favorable tax rates, they still count toward MAGI.

This surprises many retirees. A portfolio sale that seems tax-efficient can still raise Medicare costs two years later.

Selling appreciated investments to rebalance, fund a home purchase, or raise cash for expenses can push income just over an IRMAA threshold—and even $1 over the line increases premiums for the entire year.

Instead of realizing gains all at once, retirees can manage MAGI by controlling timing:

- Spread gains over multiple years

- Use tax-loss harvesting to offset gains

- Sell during low-income years (often right after retirement)

- Coordinate gains with planned Roth conversion years

- Maintain a cash reserve to avoid forced sales

IRMAA planning is not about minimizing taxes each year—it’s about managing income across many years. A strategy that looks tax-efficient in one year may increase lifetime Medicare costs if it repeatedly pushes income above thresholds.

WealthTrace Planning Tip: Use WealthTrace to model when to realize capital gains. By comparing different sale years and coordinating with Roth conversions, you can reduce the risk of triggering higher Medicare premiums.

3

Request a New Determination After Life-Changing Events

If income drops significantly due to retirement, divorce, job loss, or the death of a spouse, you may qualify for an IRMAA adjustment.

You can file Social Security Form SSA-44 to request a new premium determination based on your current income rather than the prior tax year used to calculate your premium.

Many retirees don’t realize this option exists and continue paying higher premiums unnecessarily.

Turn “two-year lookback” surprises into a plan.

WealthTrace helps you model timing decisions—Roth conversions, capital-gain harvesting, and withdrawal strategies—so you can aim to avoid unnecessary IRMAA surcharges and keep more cash in your pocket.

Try WealthTrace Free

No guesswork—just clear projections.

The Bottom Line

Medicare IRMAA has become a major retirement planning factor, particularly for higher-income households. Because premiums are tied to income from two years earlier, past financial decisions can reduce today’s Social Security payment.

Fortunately, proactive strategies—prioritizing tax-free income, timing capital gains carefully, planning Roth conversions, and appealing premiums after life changes—can significantly reduce lifetime Medicare costs.

WealthTrace calculates projected Medicare premiums and IRMAA in each year of your plan, allowing you to incorporate healthcare costs into long-term retirement projections and make more informed withdrawal decisions—helping more of your retirement income stay in your pocket.