Retirement Income • Withdrawal Strategy • Tax Planning

Where Will Your Retirement Income Come From?

What to Test in the Final Five Years Before Retirement

3 Key Takeaways

1

Retirement income planning is different from saving for retirement. Once paychecks stop, the focus shifts from accumulation to creating a sustainable income stream.

2

The order of withdrawals can meaningfully affect taxes and long-term results. Testing different withdrawal strategies can help show how taxable accounts, traditional IRAs, Roth accounts, and other assets may work together.

3

Social Security, Roth conversions, taxes, and investment risk should be evaluated together. Looking at each decision in isolation can miss important tradeoffs.

Want to see where your retirement income may come from each year?

Run retirement income scenarios in WealthTrace to test withdrawal orders, Social Security claiming ages, Roth conversions, tax strategies, and market stress before you make permanent decisions.

Start Free Trial

Build a more detailed retirement income plan.

As retirement gets closer, the planning conversation often changes. For many years, the focus is usually on saving, investing, and trying to reach a target retirement number.

In the final five years before retirement, the questions become much more specific.

Where will your income come from each year? Which accounts will you draw from first? When might Social Security begin? Should Roth conversions be considered? How much could taxes affect the plan? What happens if the market declines early in retirement?

These are not questions with one universal answer. The best approach depends on income needs, account types, tax situation, investment mix, Social Security benefits, legacy goals, and comfort with risk. That is why the years leading up to retirement are an ideal time to test different strategies before making permanent decisions.

Start With Realistic Spending

Before testing withdrawal strategies, it is important to have a realistic estimate of retirement spending. This should include essential expenses, discretionary spending, healthcare, insurance, travel, home repairs, taxes, and inflation.

Many people underestimate how much their spending may change in retirement. Some expenses may go down, such as commuting or payroll taxes. Others may rise, especially healthcare, travel, hobbies, or home improvement costs.

The first few years of retirement can also be more expensive if retirees are healthy, active, and eager to enjoy their new flexibility.

WealthTrace Planning Tip: Use detailed expense inputs to separate essential spending from discretionary spending. This can make it easier to see which expenses must be covered in all market environments and which could be adjusted if needed.

Decide When Each Income Source Begins

A retirement income plan usually includes multiple income sources. These may include Social Security, pensions, part-time work, annuities, taxable accounts, traditional IRAs, Roth accounts, and cash reserves.

The timing matters. Starting Social Security earlier may provide income sooner, while delaying may increase the monthly benefit. Drawing from taxable accounts first may reduce near-term taxes, while using traditional IRAs earlier could lower future required minimum distributions.

Roth accounts may be valuable later in retirement because qualified withdrawals are tax-free.

There is no single best order for everyone. A strategy that works well for one household may not work as well for another.

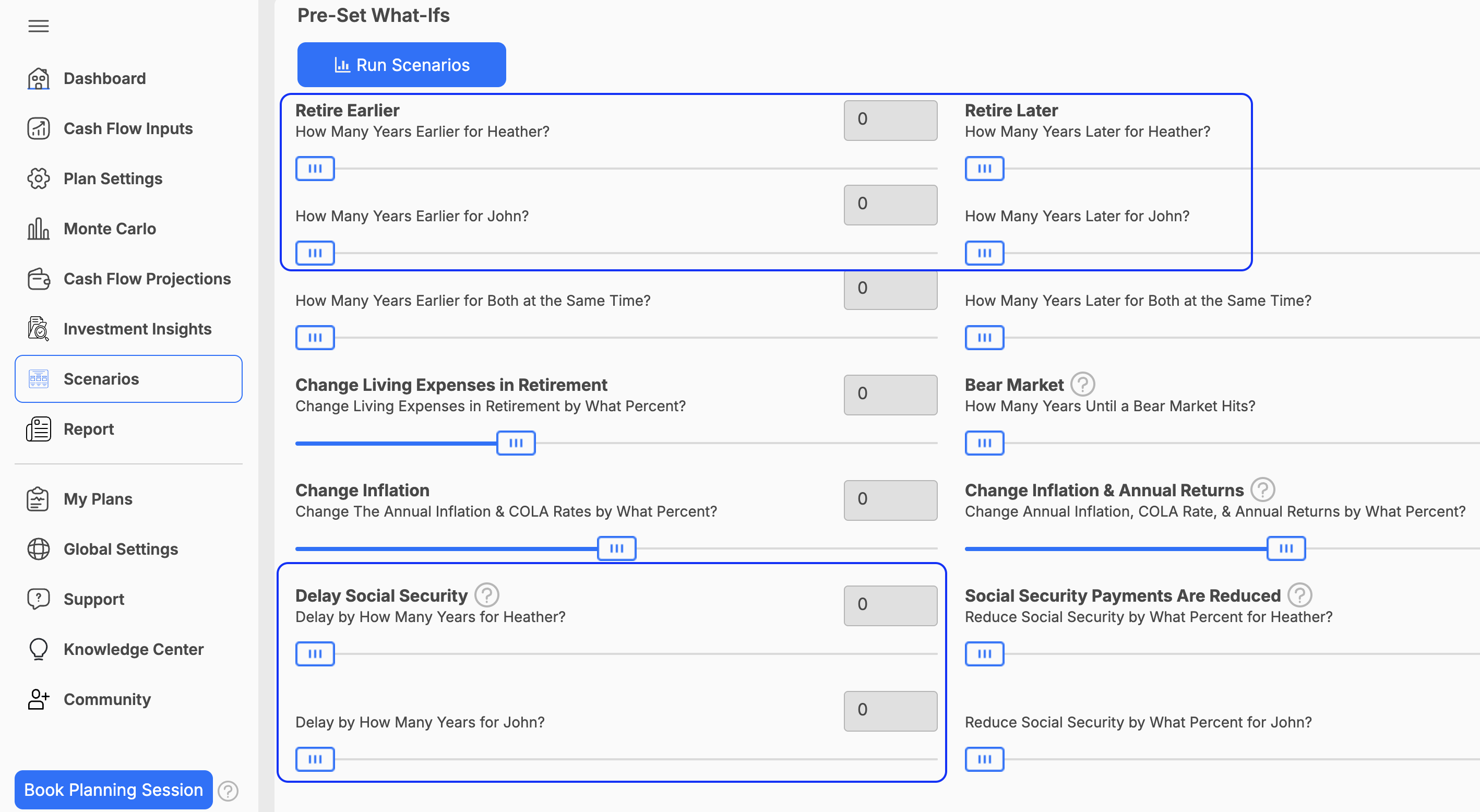

WealthTrace Planning Tip: Create multiple scenarios to compare different Social Security claiming ages, pension start dates, retirement dates, and account withdrawal orders. You can run Social Security and retirement date scenarios in the Scenarios section and control withdrawal rules and order under Cash Flow Inputs > Investment Accounts. This can help show how each approach affects taxes, portfolio longevity, and ending balances.

Test Different Withdrawal Strategies

One of the most important questions before retirement is which accounts to withdraw from first.

A common approach is to use taxable accounts first, then tax-deferred accounts, then Roth accounts. But this default order is not always the most efficient.

In some cases, drawing from tax-deferred accounts earlier may help reduce future RMDs. In other cases, preserving Roth assets may provide valuable flexibility later.

Some retirees may benefit from blending withdrawals across account types to manage tax brackets over time.

The key is not to guess. It is better to model several approaches and compare the results.

WealthTrace Planning Tip: Use WealthTrace to test different withdrawal methods and compare how they affect annual taxes, account balances, RMDs, and the overall probability of plan success.

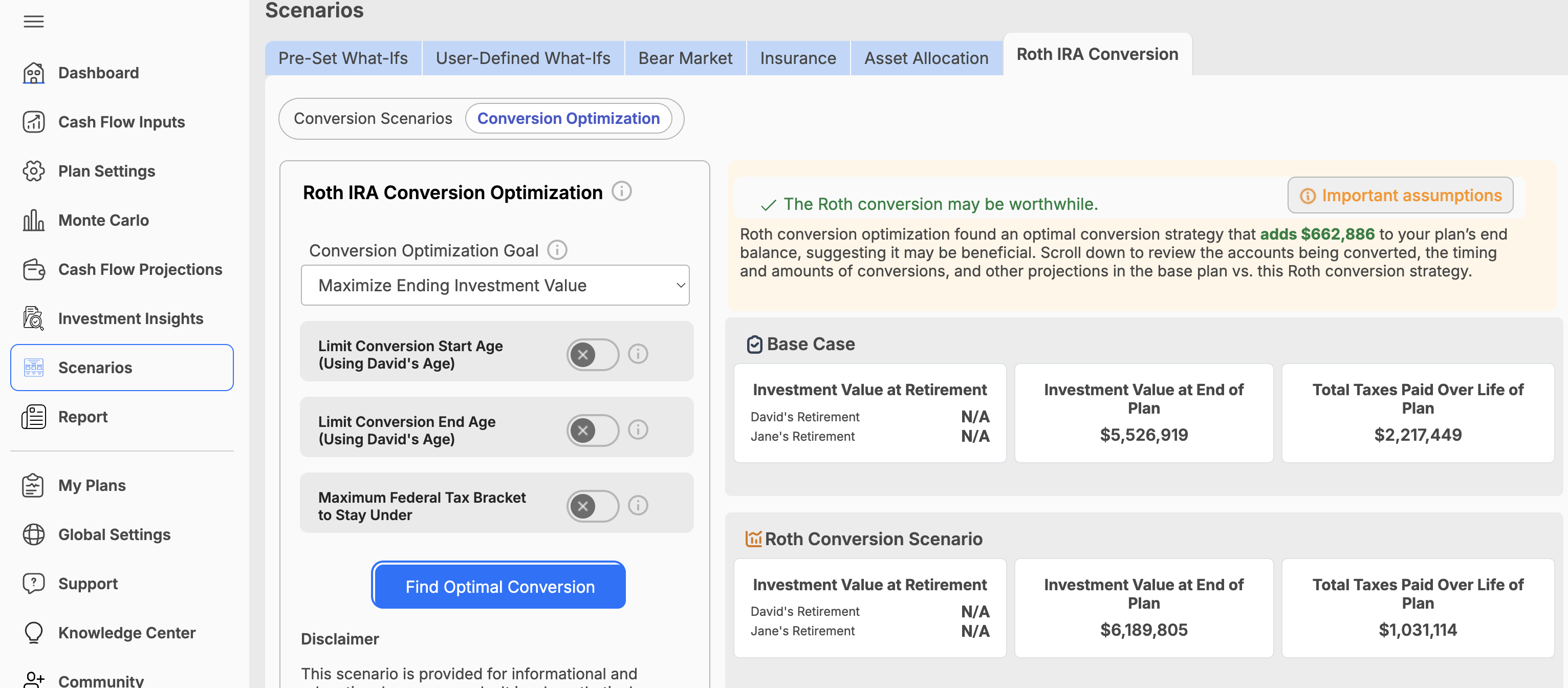

Look for Roth Conversion Opportunities

The years between retirement and the start of Social Security or RMDs can sometimes create a lower-income window. During that period, Roth conversions may be worth evaluating.

A Roth conversion means moving money from a traditional IRA or other pre-tax account into a Roth IRA and paying tax on the converted amount.

This can increase taxes in the year of conversion, but may reduce future tax-deferred balances, lower future RMDs, and create more tax-free income flexibility later.

That does not mean Roth conversions are always beneficial. They can increase current taxes, affect Medicare premiums, and may not be worthwhile if future tax rates are lower than expected.

This is why testing different conversion amounts and years can be helpful.

WealthTrace Planning Tip: Use the Roth Conversion tools to compare scenarios with no conversions, annual conversions, or targeted conversions up to a certain tax bracket. Review not just ending portfolio value, but also lifetime taxes, RMDs, and Medicare premium impacts where applicable.

Test your retirement income strategy before retirement begins.

WealthTrace helps you compare withdrawal orders, Roth conversion strategies, Social Security timing, taxes, and retirement income sources so you can better understand the tradeoffs before making big decisions.

Start Free Trial

Compare retirement income scenarios instantly.

Stress-Test the Plan

The final five years before retirement are also a good time to evaluate risk. A plan may look strong under average market returns, but retirement rarely unfolds exactly as expected.

Important stress tests may include:

- A bear market early in retirement

- Higher inflation

- Lower investment returns

- Unexpected healthcare costs

- Higher spending in the first decade of retirement

Sequence-of-returns risk is especially important because poor market returns early in retirement can have a larger impact than the same returns later.

WealthTrace Planning Tip: Run Monte Carlo simulations, bear market scenarios, and inflation adjustments. Compare how different withdrawal strategies perform under both average conditions and difficult market environments.

Review the Plan Annually

A retirement income plan should not be built once and then ignored. Markets change, tax laws change, spending changes, and personal goals change.

Reviewing the plan each year can help retirees decide whether to adjust withdrawals, rebalance investments, delay or start income sources, or update Roth conversion plans.

The goal is not to predict every outcome. The goal is to build a flexible plan and understand the tradeoffs before decisions need to be made.

The Bottom Line

The final five years before retirement are an important time to move from a general savings goal to a detailed income strategy.

Instead of asking only whether you have enough, it can be helpful to ask where income will come from, how taxes may affect withdrawals, and how the plan may hold up if conditions change.

WealthTrace can help users test different approaches, including withdrawal orders, Social Security claiming ages, Roth conversions, inflation assumptions, bear markets, and Monte Carlo results. While no software can determine the perfect strategy for every person, modeling these decisions can make the tradeoffs clearer and help retirees approach the transition with more confidence.