Roth Conversions • Tax Planning • Retirement Strategy

Roth Conversion Optimization: A Smarter Way to Plan Your Strategy

3 Key Takeaways

1

Roth conversion planning is not just about deciding whether to convert. It is about finding the right timing, annual conversion amounts, and overall objective.

2

Manual scenarios are useful when you want to test a specific strategy, but they can require several rounds of comparison.

3

WealthTrace’s Roth Conversion Optimizer can help identify a strategy based on what matters most to you, whether that is maximizing ending investment value, minimizing lifetime taxes, or maximizing the value left to heirs.

Want to find a smarter Roth conversion strategy?

Use WealthTrace to test Roth conversion scenarios, compare tax impacts, evaluate future RMDs, and optimize your strategy based on your retirement income and legacy goals.

Start Free Trial

Compare Roth conversion strategies instantly.

Roth Conversion Planning Has Changed

For years, Roth conversion planning has centered around one basic question: should I convert money from a traditional IRA or 401(k) into a Roth account?

That is still an important question. But for many retirees and near-retirees, the better question is more specific: how much should I convert each year, when should those conversions happen, and what outcome am I trying to improve?

A Roth conversion can create meaningful long-term benefits, but only if it fits into the rest of your retirement income plan. Converting too much in one year can increase taxes, push income into a higher bracket, or trigger higher Medicare premiums. Converting too little may leave more money in tax-deferred accounts, which can lead to larger required minimum distributions later.

This is why Roth conversion planning is less about one isolated calculation and more about building a multi-year strategy.

Why Timing Matters So Much

The most attractive Roth conversion opportunities often appear during lower-income years.

For example, someone may retire at 60 but delay Social Security until 67. During those years, taxable income may be lower than it was during their working years and lower than it will be once Social Security and required minimum distributions begin.

That window can create an opportunity to convert some pre-tax retirement savings at a lower tax rate. But the right amount to convert may change each year depending on expenses, withdrawals, investment income, tax brackets, Social Security timing, and Medicare premium thresholds.

This is where a simple calculator often falls short. A single-year estimate may show the tax cost of one conversion, but it does not show how that decision affects the rest of your retirement plan.

WealthTrace Planning Tip: Look for lower-income years before Social Security, required minimum distributions, or other income sources begin. These years may create an opportunity to evaluate Roth conversions as part of a broader retirement income and tax strategy.

Manual Roth Conversion Scenarios Still Have Value

In WealthTrace, users can run manual Roth conversion scenarios when they want to test a specific strategy.

This can be helpful if you already have a plan in mind. For example, you may want to convert a set dollar amount each year, stop conversions when Social Security begins, or stay within a certain tax bracket.

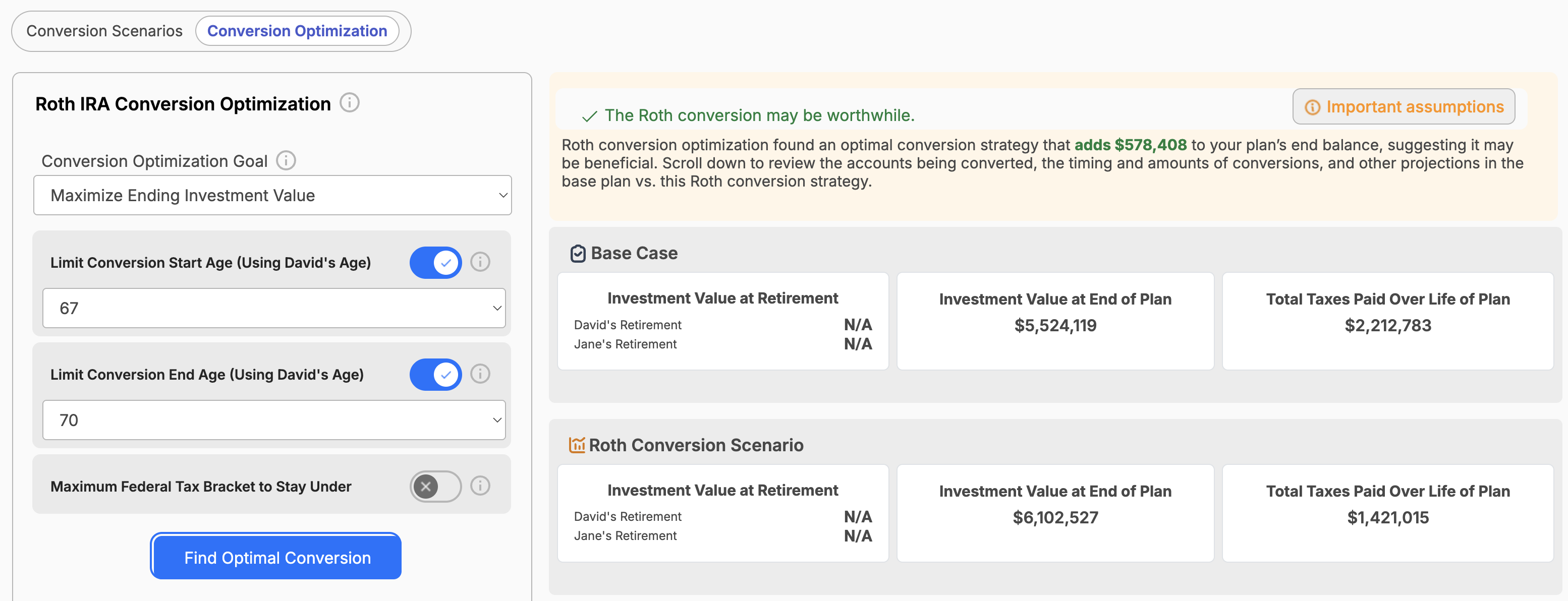

The manual Roth conversion tool gives you control over the assumptions you want to test. In this example, the user can select the account to convert from, choose a method for determining conversion amounts, set the start age, and decide how many years the conversion strategy should run.

This approach is especially useful when you want to answer questions like:

- What happens if I convert $50,000 per year for five years?

- Should I convert before Social Security begins?

- How would a larger conversion affect my taxes this year?

- Would spreading conversions out improve my long-term results?

Manual scenarios are useful when you know what you want to test. However, if you are trying to find the most efficient strategy, you may need to compare several different timelines, amounts, and tax bracket targets before deciding which approach works best.

WealthTrace Planning Tip: Use manual Roth conversion scenarios when you want to test a specific amount, time period, account, or tax bracket target. This can be useful when you already have a strategy in mind and want to compare it against your base plan.

Where the Roth Conversion Optimizer Helps

The Roth Conversion Optimizer is designed to make that process more efficient.

Instead of manually testing one conversion strategy at a time, you can choose an objective and set constraints. WealthTrace then helps determine a conversion strategy that best fits those inputs.

Depending on your goals, you can choose to optimize for:

- Maximizing ending investment value, which focuses on improving long-term after-tax wealth

- Minimizing lifetime taxes, which focuses on reducing total taxes paid over your lifetime

- Maximizing investment value for beneficiaries, which focuses on increasing the after-tax value your heirs may receive

This is an important distinction. Not every Roth conversion strategy is trying to solve the same problem. A strategy that minimizes lifetime taxes may not be identical to a strategy designed to leave the most after-tax value to heirs. The optimizer gives you a way to align the analysis with your actual planning priorities.

You can also set limits around the strategy, such as the age range when conversions should occur or the maximum federal tax bracket you want to stay under. This gives the optimizer structure while still allowing WealthTrace to identify a strategy that may be more efficient than manually testing different combinations.

WealthTrace Planning Tip: Use the Roth Conversion Optimizer when you want WealthTrace to help identify a strategy based on your objective, age range, and tax bracket limits instead of manually testing one conversion plan at a time.

Optimize Roth conversions based on what matters most to you.

WealthTrace lets you compare manual Roth conversion scenarios and optimized strategies based on investment value, lifetime taxes, and potential value left to heirs.

Start Free Trial

Run Roth conversion scenarios today.

Why the Optimizer Can Be More Useful Than a Stand-Alone Calculator

A Roth conversion does not happen in isolation. It interacts with several other parts of a retirement plan.

A conversion may affect federal taxes, state taxes, taxable Social Security, Medicare premiums, required minimum distributions, withdrawals, capital gains, and future account balances. These items are connected, and a decision that looks good in one year may not be ideal over the full retirement timeline.

Because the Roth Conversion Optimizer is built into WealthTrace, it evaluates conversions within the context of the full plan. That means the results are not based only on one conversion amount or one tax year. They reflect how the strategy may affect income, taxes, and account balances over time.

This is especially important for retirees who are trying to manage taxes across several stages of retirement, including the years before Social Security, the years before required minimum distributions, and later retirement years when income sources may change.

WealthTrace Planning Tip: Evaluate Roth conversions alongside Social Security timing, Medicare premium thresholds, RMDs, withdrawals, capital gains, and future account balances so the strategy reflects the full retirement plan rather than a single tax year.

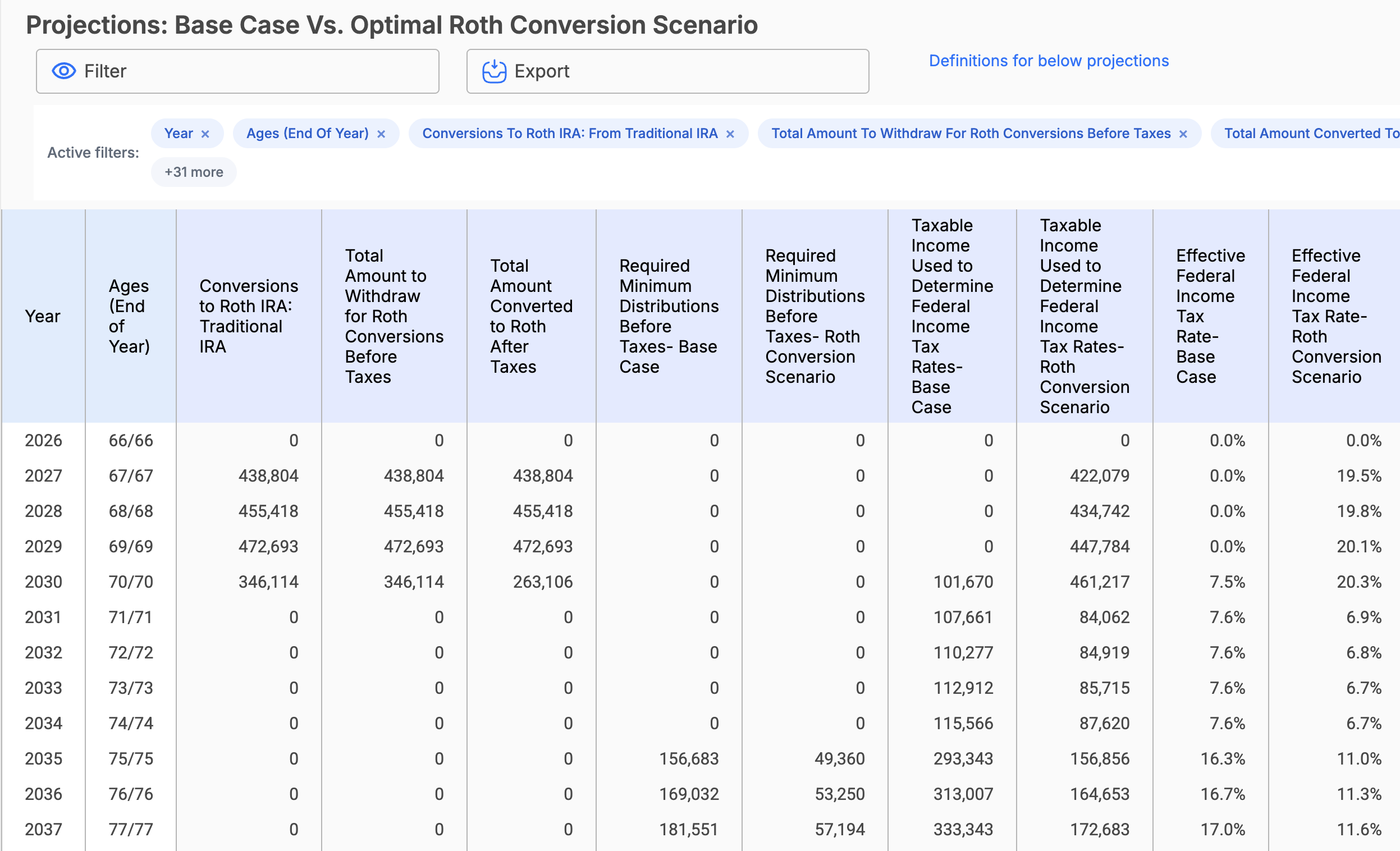

Comparing the Results

After running a Roth conversion scenario or optimization, WealthTrace shows how the strategy compares to the base case across several key areas.

The results can help you see how the conversion strategy affects investment balances, cumulative taxes paid, marginal tax rates, and required minimum distributions over time. In this example, the optimized conversion strategy increases the ending investment balance, lowers cumulative lifetime taxes, and reduces future required minimum distributions compared to the base case.

This type of side-by-side comparison is useful because Roth conversions often involve tradeoffs. A strategy may increase taxes in the early conversion years but reduce taxes and required minimum distributions later. Seeing those effects visually can make it easier to understand whether the conversion strategy is worthwhile.

WealthTrace Planning Tip: Compare the optimized strategy against the base case by reviewing ending balances, cumulative taxes, tax rates, and required minimum distributions. Roth conversions often involve short-term tax costs, so the long-term comparison is what matters most.

The Bottom Line

Roth conversions can be powerful, but the best strategy is rarely as simple as converting a fixed amount or using a one-year calculator.

The timing, annual conversion amount, tax limits, and optimization goal all matter. So do Social Security, Medicare premiums, required minimum distributions, state taxes, capital gains, and future withdrawals.

Manual scenarios can help you test specific ideas, but WealthTrace’s Roth Conversion Optimizer can make the process more efficient by helping identify a strategy based on your plan, your constraints, and your priorities.

Instead of relying on trial and error, you can use optimization to evaluate Roth conversions as part of a broader retirement income, tax, and legacy strategy.