It has been a question for as long as people have thought about retirement: How much can one withdraw from his or her portfolio each year without running out of money in retirement?

Before the two bear markets in the last decade, many financial advisors simply told their clients to take out a percentage of their portfolio that is close to their expected returns. That way they’ll never run out of money. If they expect a 5% after-tax return, then they withdraw 5% per year and don’t have to worry about anything. Of course, there is more than one problem with this line of thinking, the first being that 5% after-tax returns per year did not happen for the vast majority of investors over the past ten years. And with treasury rates hovering near 0%, many baby boomers approaching retirement or already in retirement are fighting just to beat inflation.

I believe that using a percentage rule for withdrawing retirement funds is not only too simplistic, it’s dangerous and unrealistic. To start with, if a couple in retirement is told to withdraw 5% per year in retirement and is generating only 2% per year in total returns, their level of spending must be reduced every single year. Let’s look at an example of a couple that has $1 million when they retire, are told they can withdraw 5% per year, and they earn 2% per year on their investments. For the sake of simplicity in this example we won’t include social security or pension payments.

| Year | Portfolio Value | Spending |

| 0 | 1,000,000 |

| 1 | 970,000 | 50,000 |

| 2 | 940,900 | 48,500 |

| 3 | 912,673 | 47,045 |

| 4 | 885,293 | 45,634 |

| 5 | 858,734 | 44,265 |

| 6 | 832,972 | 42,937 |

| 7 | 807,983 | 41,649 |

| 8 | 783,743 | 40,399 |

| 9 | 760,231 | 39,187 |

| 10 | 737,424 | 38,012 |

In just ten years this couple will have to spend nearly $12,000 less than they were spending when they started. Who wants to watch their standard of living decline each year? That is precisely what they’re being asked to do though. By holding to a rigid percentage rule, they have to spend less and less each year.

Most people very much dislike the notion of changing consumption patterns. Much research has been done on the idea of consumption smoothing and I believe it is one way in which people can increase their overall well being in retirement. In other words, most of us to prefer to spend nearly the same amount every year, especially once we retire.

Another important point that is not discussed nearly enough when it comes to these types of rules is this: many retirees don’t want to maintain their portfolio value by living frugally. They want to enjoy their retirement by spending down the income and principal in their portfolio. As long as they don’t run out of money in retirement, they’re happy. There is such a thing as spending too little in retirement.

Regardless of whether or not one believes consumption smoothing is a good idea or whether or not percentage based retirement rules are a good idea, the point is now moot. Percentage based retirement rules simply will not work for most people in retirement, especially if they have a heavy weighting in fixed-income (which most retirees do), and are not achieving a total return of even 2%.

As I’ve said to co-workers before, it’s easy to find complaints, but what is the solution? I’ve done my complaining about the percentage retirement rule and now here is my solution: Most people building a retirement plan should be using a dollar based rule that is dependent on their own goals and net worth. By using a dollar based rule, retirees can spend the same amount, or nearly the same amount, each year without worrying about having to reduce their standard of living each and every year.

It takes a little more work and very likely a financial planner or a very goodretirement calculator, but a dollar based rule is the best solution for most people today. Setting up this rule requires not only inputting all of your financial data, it also requires a conservative approach in my opinion. You don’t want to choose the scenario where you expect 8% returns per year, which shows a safe level of spending of $50,000 a year, only to run out of money when you’re 80 because the stock market had another lost decade.

Also keep in mind that the dollar amount I am talking about here is always in inflation-adjusted terms. The goal is to spend a relatively constant amount in real dollars each year in retirement.

I believe it is of utmost importance to choose a relatively pessimistic scenario of returns that only equal inflation or are even worse than inflation. I also believe that when using this rule, one must have a very large buffer in terms of when they run out of money. When I generate my own retirement plan, I want an annual spending figure in retirement that gives me until I’m at least 110 years old before I run out of money.

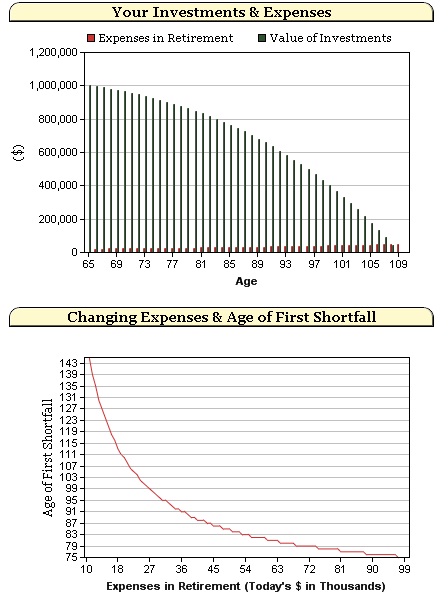

Let’s go back to the example used earlier of the couple with $1 million in savings when they retire. Using my calculator called How Changing Expenses Affect Your Retirement, which is freely available to anybody, I started off by assuming a 2% annual return and a 2% annual rate of inflation. I also assumed both people are 65 and have just retired. I inputted expenses of $45,000 per year. With these assumptions, and taking into account taxes on withdrawals, this couple would run out of money when they’re 86 years old. That is way too early for my taste. Like I said before, I want to see my money stick around until I’m at least 110. By running a few more scenarios I found that this couple can spend $20,000 a year in retirement and their money won’t run out until they’re 110 years old. It’s also important to keep in mind that social security and any other cash sources are not taken into account here. That would of course increase the amount they can spend per year.

It is also important to point out that by calculating what this couple can safely spend in retirement early on, they can change their behavior today in order to make their retirement more enjoyable. If they think the dollar amount they can spend each year in retirement is way too low, perhaps they can save more today, cut back on expenses today, or retire at a later date. No matter which path they choose, it is unfair to people approaching retirement to tell them that they should just choose a percentage value to withdraw each year and stick with it. With today’s retirement planning tools, they can do much better than that.