There are so many strategies for investors that are tossed around these days that it’s easy to forget one of the most important ideas: Those who are younger should be taking more risk in their retirement portfolios than those who are approaching retirement. There are a few reasons for this. First, those of us who won’t retire for another 25 years simple won’t need the money in our retirement accounts any time soon. So the day to day gyrations in the markets have much less impact on our levels of stress and our decision making. Second, because younger folks are much less concerned about day to day movements in their retirement portfolios, they are much less likely to panic and move in and out of the market. And lastly, it has been proven again and again that given enough time, higher risk means higher returns. The key phrase here is “given enough time”.

I like to compare the risk vs. reward tradeoff to how a casino makes money. A blackjack table at a casino in Las Vegas might lose money in the first hour of the night. They might even lose money all night long. And sometimes, they might lose money for the week. But it is an absolutely guarantee that, short of some type of cheating or incredible card counting taking place, the casino will make money on that blackjack table over the year.

Similar to the casino, the odds are normally in investors’ favor over the long-run. But it’s not as simple as it is for the casino. There are many ways to lose money as an investor, even over a 25 year time frame. The key is to have a solid strategy for your retirement, stick to the strategy, and diversify your holdings. Given this, let’s look at a retirement portfolio for those under 40 years old that I have recommended for a few years now.

Solid dividend paying stocks- The core of the portfolio:

The core of my retirement portfolio is a foundation of dividend paying stocks that have had consistent dividend growth over time as well as low payout ratios and low debt. I wrote about this strategy a year ago and it has done quite well so far. Five of the companies that make up this part of the portfolio are Johnson & Johnson (JNJ), Procter & Gamble (PG), Coca-Cola (KO), Exxon (XOM), and Sysco (SYY).

| Company | Div Yield | 1 Yr Div

Growth Rate | 1 Yr Div

Growth Rate | Payout Ratio | Debt/Equity |

| JNJ | 3.5% | 9.3% | 10.6% | 54.0% | 29.8% |

| PG | 3.1% | 9.3% | 11.4% | 51.0% | 51.5% |

| KO | 2.7% | 7.3% | 9.5% | 34.0% | 87.0% |

| XOM | 2.2% | 4.8% | 8.8% | 22.0% | 10.3% |

| SYY | 3.7% | 4.0% | 9.3% | 40.0% | 55.8% |

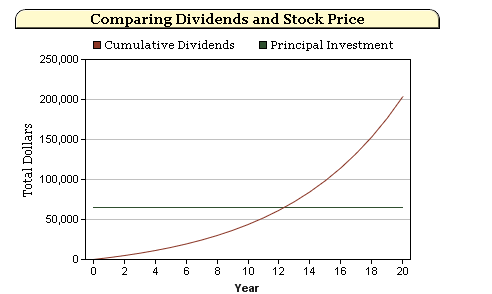

Besides having in common their relatively strong dividend yields and growth rates, these companies have also shown a commitment over long periods of time to keep growing their dividends. Over time, consistent dividend growth will lead to solid total returns even if stock prices fall during the investing period. To show this I ran an example using our publicly available calculator called Total Returns- Dividends vs. Price Appreciation. I took 1,000 shares of Johnson & Johnson (JNJ) at today’s price and assumed a growth rate of dividends of 10%. Over 20 years we see the following:

Even if the stock price doesn’t budge over the 20 year time frame, we would see a 313% total return (7.3% annual return). Like I said before, the movements in the stock price over a time period this long become nearly meaningless to those collecting the dividends.

Take more risk in your tax-deferred accounts:

The second part of the strategy is to take more risk while you’re young, especially in a tax-deferred account. If it’s an account you cannot access until you retire, you are much less likely to be affected mentally by the wild volatility that riskier investments can have. In fact, younger people should not be looking at their retirement portfolio’s value every week or even every month.

In terms of taking risk, I’m talking about emerging markets and even frontier market funds. We all have so much more access to investing in other countries today than we did 10 years ago. There are many Exchange Traded Funds to choose from, such as the iShares Emerging Markets ETF (EEM) and the Guggenheim Frontier Markets ETF (FRN). Investors even have access to investing in countries like Vietnam (VNM) as well as the continent of Africa (AFK).

Investing in riskier assets can be a serious boost to your portfolio over time. It’s always astonishing to me when I see just how big of an impact a 1% or 2% return increase per year can have on a portfolio. Let’s say a 35 year old investor has $100,000. It is sitting in bonds in his retirement portfolio. He decides to move this portion to emerging markets and frontier markets. Using our free calculator called 401(k) Benefits, I calculated the following:

| Annual Return | Investment Value | Difference From

2% Return |

| 2% | $148,595 | 0 |

| 3% | $180,611 | $32,016 |

| 4% | $219,122 | $70,527 |

| 5% | $265,330 | $116,735 |

| 6% | $320,714 | $172,119 |

| 7% | $386,968 | $238,373 |

Keep non-qualified dividends in your tax-deferred retirement account:

I have written before on the topic of how to allocate investments between taxable and tax-deferred accounts. One idea I normally recommend to people is to hold high-dividend paying REITs and even Master Limited Partnerships (MLPs) in their tax-deferred retirement accounts. Both REITs and MLPs are subject to the full income tax rate in taxable accounts. And because they pay out so much in dividends, you cannot time when to pay taxes like you can with capital gains.

I currently have a substantial holding of Annaly Capital Management (NLY) in my tax-deferred IRA precisely because it pays a 14% dividend yield, which is taxable at my full marginal income tax rate. It is also important to point out that MLPs have more complex tax rules and there is a limit to how much you can have in a tax-deferred account.

Following the three strategies I’ve highlighted above can help secure your retirement over the long-run. But it’s important to start saving your retirement while you’re relatively young so you can take more risk and reap the rewards of compounded returns over time.

Retirement Planning Software | Financial Planning Software