As I write this Apple's (AAPL) stock is down 42% from its peak of $705 a share. It has been a brutal nosedive for those who recently bought Apple hoping they would see some of the tremendous gains that other investors have over the past four years.

But those who are looking at the long-run dividend potential of Apple are cheering the fall in its stock price. Because of this decline Apple's dividend yield is now a respectable 2.5%. But more than that, Apple has the ability to increase its dividend at a very healthy clip for years and even decades to come.

Apple has an astonishing $137 billion in cash on hand. That works out to $145 per share of stock. Also, its payout ratio (the fraction of net income paid as dividends to shareholders) is a very low 12%. These two facts set Apple up as a potential stellar dividend payer for many years.

What I want to look at in this article is how a company like Apple can change (and potentially save) a retirement portfolio. I want to show what the dividends alone can potentially achieve over a long time horizon.

After stopping dividend payments in 1995, Apple just began paying a dividend once again in August of last year. They have yet to announce what their dividend increase will be for this year. So we need to make a projection of how much Apple can (or will) increase its dividend in the years to come.

Let's take a look at how Microsoft, another technology giant that is paying dividends, has increased its dividend over the years. Over the past 10 years Microsoft has increased its dividend by an average of 11% per year. But this does not take into account the enormous special dividend that it paid out in 2004. Taking this into account they actually increased their dividend by an average of 350%.

What about Intel? We have 20 years of dividend history for this company and they have averaged an increase of 31% per year in their dividend payments.

So let's look at a scenario where we add a company like Apple to a retirement portfolio.

I want to take a look at a 45 year old couple that has been scared out of the stock market and currently has everything invested in long-term treasury bonds yielding 2.8%. They currently have $400,000 saved and are saving $10,000 per year. Let’s also apply an inflation rate of 2% for each year. They plan on retiring when they are 65. How much money can they expect to have when they retire if we take into account inflation? For this example I assumed half of their money was in a qualified, non-taxable account such as an IRA. They pay taxes at a 30% rate on their investment income and dividends are taxed at a 15% rate. They plan on spending $50,000 per year in retirement. Lastly, they expect to receive combined social security payments of $35,000 per year when they are 67.

Here are the results for this couple if they keep all of their money invested in low-yielding treasuries:

| Beginning Value

Of Account | Value

Of Account At Retirement (Nominal $) | Value

Of Account At Retirement (Real $) | Real Annual Return After Taxes |

| $500,000 | $640,000 | $545,890 | 0.57% |

In 20 years their investments have only grown by a mere $45,890 if we reduce everything by the inflation rate. That is only 0.57% per year in real terms. I plugged in these numbers into our Retirement Planner and found that this couple would only have a 15% chance of not running out of money if they save $10,000 a year for the next 20 years, spend $50,000 a year in retirement and receive $35,000 a year in social security payments. This couple is headed for serious trouble.

Now let’s look at the case where they invest half of their money in a basket of dividend paying stocks like Apple. It is important to note that I am not recommending investing in just one stock. I am recommending investing in a basket of solid dividend paying stocks that are projected to pay growing dividends for a long period of time.

In this example I assumed a dividend yield of 2.5%, long-term dividend growth of 15%, and no increase in the stock price at all. I ran these numbers in our free online calculator called Dividend Yield And Growth.

| Beginning Value

Of Account | Value

Of Account At Retirement (Nominal $) | Value

Of Account At Retirement (Real $) | Real Annual Return After Taxes |

| $500,000 | $1,250,000 | $885,400 | 5.2% |

Now we’re talking some real money when they retire. They will have over $885,000 (in today’s dollar terms) when they retire. Plugging these numbers into our Retirement Planner I found that they now have a 90% chance of never running out of money in retirement. It is important to keep in mind that I assumed no change in the stock price in this example. I wanted to show how just collecting the dividends from strong dividend growth stocks can have such a large impact.

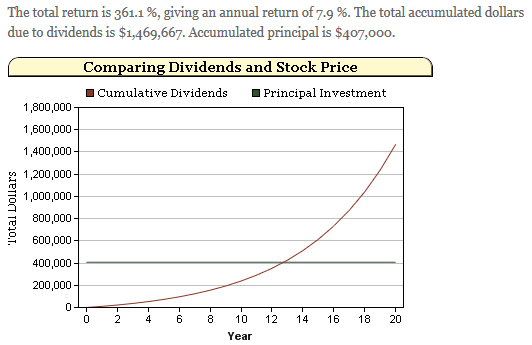

In fact, with a company like Apple, where we expect them to increase their dividend at a rapid rate for years to come, the change in the stock price becomes nearly meaningless. If you invested in 1,000 shares of Apple today, the dividend growth rate is 15% per year, and their stock price doesn't move, we see the following over 20 years:

Notice how the dividend payments eventually swamp the initial investment. In fact, the stock price could fall by 50% over this time frame and the investor would still see an annual rate of return of 6%.

Given enough time, a company like Apple can completely change the retirement picture for an investor. Of course, this assumes that they will increase their dividend payments by relatively large amounts over time. But if history is any guide, companies like Apple will indeed reward shareholders with large increases in dividends. Perhaps more importantly, no company has the ability to pay hefty dividends as much as Apple does.